Your insurer sends an Explanation of Benefits after every claim. Most people glance at it, assume it’s a bill, and file it away. That’s a costly mistake. Knowing how to understand an explanation of benefits statement is one of the most practical skills you can develop as a patient or practice manager. An EOB tells you exactly what was billed, what your plan allowed, what the insurer paid, and what you legitimately owe, information you can use to catch billing errors, identify underpayments, and push back on denials with confidence.

This guide walks through every section of an EOB statement in plain English, with a real-world example and clear next steps so you never misread one again.

What an EOB Is (and What It Isn’t)

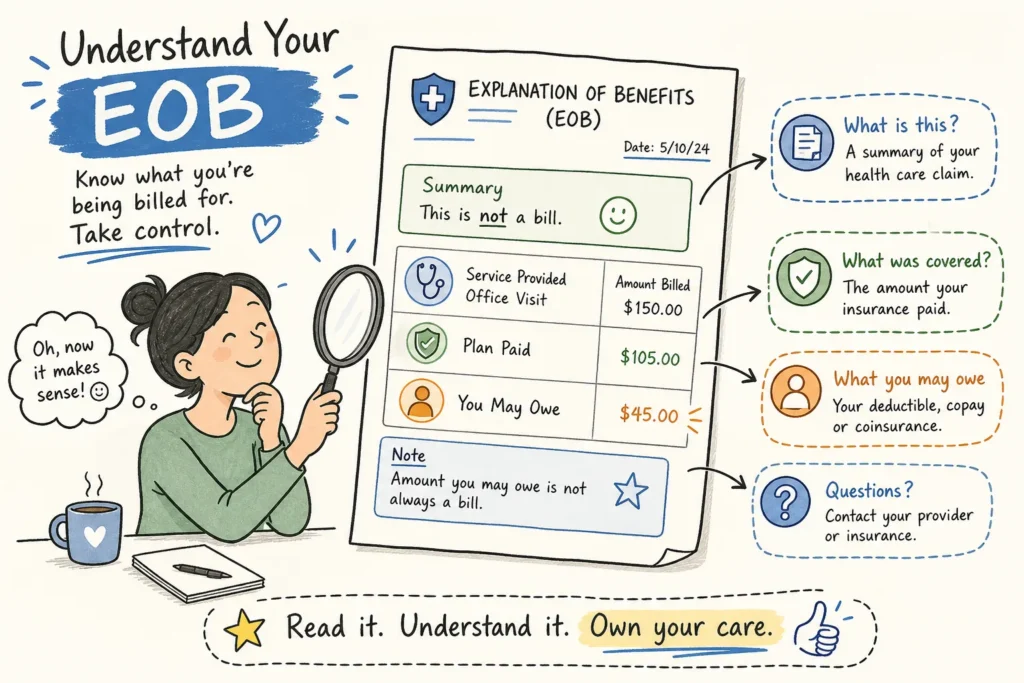

An Explanation of Benefits is not a bill. It is a statement from your health plan explaining how a claim was processed. You receive it after your provider submits a claim to your insurer, and it shows the insurer’s decision on that claim, not a demand for payment. Confusing the two leads patients to either pay more than they owe or ignore a balance they actually do owe.

For patients, the EOB confirms whether the insurer applied your benefits correctly. For medical practices, the EOB, or its provider-side equivalent, the remittance advice, is the primary tool for catching claim errors, underpayments, and denials before they become write-offs. Both documents carry the same core financial data, so understanding how to read one teaches you to read the other.

How to Understand an Explanation of Benefits Statement: Key Sections

The top of every EOB identifies the patient by name and member ID, names the provider who submitted the claim, and assigns a unique claim number. That claim number is critical: keep it handy whenever you call the insurer about a specific service. Without it, customer service representatives often can’t locate the right claim quickly, which wastes time and delays resolution.

The billed amount (also called provider charges or total charges) is what your provider asked the insurer to pay. The allowed amount is what the insurer has agreed to recognize under its contract or pricing rules. These two numbers are almost never the same. The difference between them is called a contractual adjustment or network discount, and in-network providers are contractually prohibited from billing you for that gap.

After that adjustment is applied, the EOB shows the insurer’s payment: the portion of the allowed amount covered by your plan. What remains goes into the patient responsibility column, the only figure you should ever pay from a provider bill. Everything else is either covered by your plan or written off under the provider’s network contract.

Decoding the Patient Responsibility Column

Patient responsibility is not a single charge. It is the sum of several cost-sharing buckets, and a well-structured EOB breaks each one out separately so you can verify that your plan applied the right amounts for your current coverage year.

Deductible

Your deductible portion is the amount applied toward your annual deductible limit. Until that limit is met, most plans require you to cover a larger share of each service’s allowed amount.

Copay

A copay is the fixed fee your plan assigns to certain visit types, a flat $30 for a primary care visit, for example, regardless of what the provider billed.

Coinsurance

Coinsurance is your percentage share of the allowed amount once the deductible is met. If your plan pays 75%, you owe the remaining 25% of whatever the insurer recognized as the allowed amount.

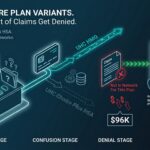

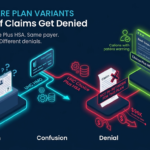

Some services show up in a “not covered” or “not eligible” column. This happens when a service is explicitly excluded from your plan, billed with a procedure code that doesn’t match your diagnosis, or delivered outside your network in a way your plan doesn’t protect. A charge landing here is a signal to investigate. It could be a legitimate exclusion, a provider coding error, or a payer-side processing mistake. Don’t assume it’s correct until you verify.

Consider a straightforward office visit as an example. The provider bills $200, the insurer’s allowed amount is $120, producing an $80 contractual adjustment. The plan pays $90 of that $120 (75% coinsurance after the deductible), and the patient owes $30. Your EOB would show all four figures in separate columns. If the provider then sends you a bill for $200 instead of $30, that is a billing error worth disputing immediately. This kind of annotated EOB example, mapping every dollar across billed charges, adjustments, plan payments, and patient responsibility, is exactly what makes this medical claims summary so powerful when you know how to use it.

Comparing the EOB to the Provider Bill

Pull both documents side by side and match each service by date, procedure code, and description. Your provider’s bill should not exceed the patient responsibility figure on the EOB for the same service. If you see the same procedure code billed twice on the provider statement, or a charge that never appears on the EOB at all, you are looking at a duplicate charge or a claim that wasn’t submitted correctly. Request an itemized bill from the provider before paying anything you can’t verify against the EOB.

Balance billing is a specific problem worth understanding. It happens when an in-network provider tries to collect the gap between their billed amount and the allowed amount, the portion that the contractual adjustment eliminates. This is prohibited for in-network providers under their network contract, and the No Surprises Act provides additional federal protections for out-of-network emergency care and certain other services. If your provider’s bill is higher than what the EOB says you owe, call the billing office first and reference the EOB’s patient responsibility figure. If the discrepancy isn’t resolved, escalate to your insurer with both documents in hand.

Timing is a separate but related complication. Sometimes a provider bill arrives before the insurer has finished processing the claim, which means no EOB exists yet to compare it to. Confirm the EOB has been issued before assuming there’s an error. Once it has, the comparison process is straightforward: the provider bill must align with the patient responsibility column, full stop.

What Denial Reason Codes on an EOB Are Really Telling You

When a claim is denied or reduced, the EOB includes a short code in the remark or reason column. The three main group codes are CO, PR, and OA. CO (Contractual Obligation) means the adjustment is due to the contract between the payer and the provider, and the balance cannot be billed to the patient. PR (Patient Responsibility) identifies what the patient legitimately owes, typically deductibles, copays, and coinsurance. OA (Other Adjustment) covers situations that don’t fit either category and requires a closer look at the accompanying remark code for context.

Beyond group codes, the specific Claim Adjustment Reason Codes (CARCs) tell a more detailed story. Code 197 means precertification or prior authorization was absent. Code 204 means the service isn’t covered under the patient’s current benefit plan. Code 16 flags a submission error where required information is missing. Descriptions are typically printed in a key at the bottom of the EOB, and you can cross-reference the full list against the standard ANSI X12 code sets published by CMS.

A single denial code might reflect a one-time coding error. The same code appearing repeatedly across dozens of claims for the same service type points to something more systematic, a payer algorithm targeting certain procedure codes, a plan policy change that wasn’t communicated, or a contracted rate dispute. Solo practice billing staff often miss these patterns simply because spotting them requires monitoring EOBs across a high volume of claims simultaneously. Practices managing that volume should consider dedicated RCM support to catch these patterns before they compound into significant revenue loss. How to Reduce Insurance Claim Denials for Your Practice, WeBill Health works across hundreds of claims at once, which means systemic denial trends surface quickly, often before they become material write-offs.

Your Next Steps: Pay, Dispute, or Appeal

After reading the EOB, you face one of three situations. If the numbers match what you expect and align with your plan benefits, pay the patient responsibility amount shown. If the provider bill exceeds the EOB’s patient responsibility, dispute the overcharge with the provider’s billing office and reference the EOB directly. If the insurer denied a service you believe should be covered, you have the right to file a formal internal appeal.

For a health insurance appeal, you generally have 180 days from the date of the denial notice to file. Gather your denial letter or EOB, the original claim, your Summary of Benefits, relevant medical records, and a letter of medical necessity from your provider if the denial is based on medical necessity. Submit everything exactly as the insurer instructs, by mail, fax, or member portal. Keep copies of every document you send and note the name and date of any phone calls, since you may need that paper trail if the internal appeal is denied. See The Claim Appeal Process: How to Fight Denials and Win, WeBill Health for a practice-focused walkthrough of the documents and timelines you’ll want to assemble.

If the internal appeal is denied, escalation options include an external independent review organization or a complaint filed with your state insurance regulator. Decision timelines differ by claim type: urgent appeals must be decided within 72 hours, pre-service appeals within 30 days, and post-service appeals within 60 days. Knowing those deadlines helps you follow up before the window closes on a legitimate reimbursement.

Reading EOBs Is a Skill Worth Building

Mastering how to understand an explanation of benefits statement means you stop guessing and start verifying. Once you can interpret billed charges, allowed amounts, adjustment codes, and patient responsibility, most billing errors and overpayments stop slipping past unnoticed, because you know exactly what to look for. For a plain-language reference you can share with patients, see this insurer’s Explanation of Benefits resource.

For individual patients, the steps in this guide are enough to protect yourself from overpaying or missing a denial you have every right to appeal. For practices managing a high volume of claims, consistent EOB review at scale is what separates those that recover every dollar owed from those quietly absorbing avoidable losses. If your team is stretched thin and denials are slipping through, that’s a problem worth solving before it compounds. Reduce Claim Denials: 9 Proven Strategies for Your Practice, WeBill Health specializes in systematic denial prevention and recovery, particularly for high-risk specialties where payer-side patterns are hardest to catch without dedicated RCM support.